The Largest Copper Project In Africa Is Being Built - Koryx Copper (CVE:KRY)

A Deep Dive into One of Africa’s Largest Undeveloped Porphyry Projects — Backed by Proven Leadership, Fresh Capital, and Near-Term Catalysts

The most critical assets are often the most overlooked. While global headlines chase the high-flying valuations of lithium and rare earths, the true engine of the global economy is copper.

Welcome to The Mineral Strategist. Our mission is to cut through the noise and uncover the fundamental, resource-driven opportunities that will define the next era of global growth. Today, we're focusing on the king of base metals and the coming structural supply deficit.

You might think of copper as a simple proxy for global GDP, dominated by giants like Codelco and Freeport-McMoRan. But the real story for a strategist lies in the looming supply crisis, the jurisdictional risks of major producers, and the technological innovations required to unlock the next generation of mines. This analysis builds on our previous work dissecting the critical minerals space, where we uncovered opportunities such as these:

Inside this post you will find:

The Turnaround Thesis: A breakdown of how new management, led by a proven team with multiple C$100M+ exits in Namibia, has recapitalized and revitalized the giant Haib Copper Project after years of dormancy.

Project Deep Dive: An analysis of Haib’s massive scale (414Mt Indicated + 345Mt Inferred), its strategic location in mining-friendly Namibia, and the latest positive drill results that point to a larger, higher-grade resource.

Upcoming Catalysts & Economics: A look at the key milestones for 2025, including an aggressive 55,000m drill program and the delivery of a new Preliminary Economic Assessment (PEA) in Q3 that will define the project's value.

The Strategist's View: Our complete investment thesis, including a clear-eyed look at the risks (low grade, financing needs) versus the potential for a significant re-rating based on peer valuations and execution.

If you want to build a portfolio of unique, high-conviction ideas and gain an edge by understanding the powerful forces shaping the resource markets, subscribe to The Mineral Strategist and join a community of discerning investors.

Executive Summary

Koryx Copper (TSXV:KRY, NSX:KYX) is a Canadian junior mining company developing the Haib Copper Project in southern Namibia, one of the world’s largest and highest-potential porphyry copper deposits.

After years of dormancy under prior owners, new management, led by Heye Daun and Alan Friedman have revitalized the project. Haib boasts a sizable copper resource of currently 414 million tonnes Indicated at 0.35% Cu, plus 345 million tonnes Inferred at 0.33% Cu and is well positioned near infrastructure in a stable, mining-friendly jurisdiction.

Koryx has raised roughly C$50M in 2024–25 and is advancing aggressive drilling and engineering programs toward an updated Preliminary Economic Assessment (PEA) expected in Q3 2025. Catalysts that could unlock further value for the Haib project include ongoing drill results (to expand and upgrade the resource), completion of met‑test and infrastructure studies, and permitting milestones (mining license application filed, ESIA in progress).

With copper in strong demand, this combination of a large project, proven management, and near-term milestones underlies a compelling upside thesis. Key risks are the low native grade (requiring large tonnage mining), the need for substantial further financing, permitting delays, and copper price variability. We view Koryx as an early-stage copper development story trading at a deep discount to peer metrics; successful execution of drilling and studies could drive a re-rating.

Company Background

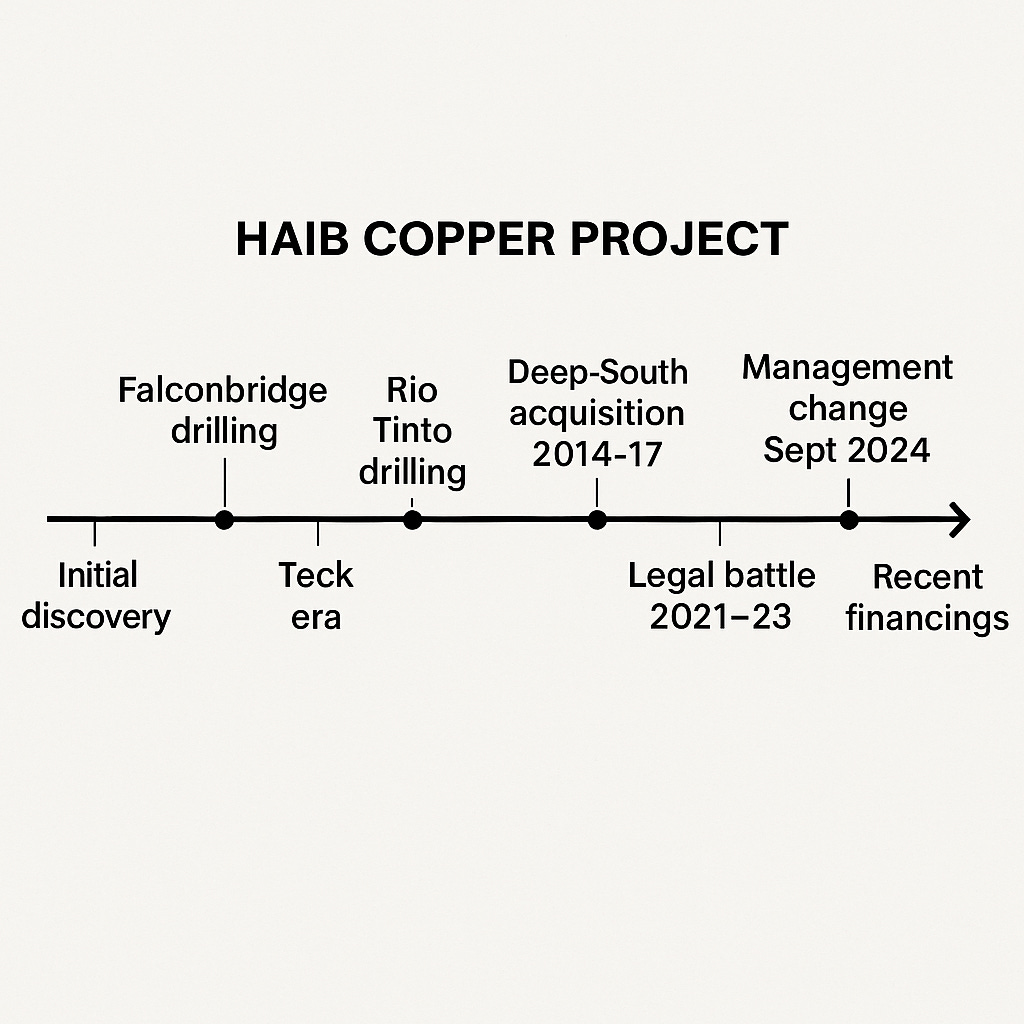

Koryx Copper traces its roots to Deep-South Resources Inc., which in 2014–2017 acquired 100% of the Haib deposit from Teck Resources via share and cash payments. Deep-South then struggled for years: it lacked funding for development, pursued a bio-leach strategy, and became embroiled (2021–2023) in a legal dispute with Namibia’s government over the Haib license.

Koryx ultimately won that case, and the Haib licence was renewed in July 2023. By early 2024 Deep-South (market cap <C$10M) had a “frustrated” shareholder base and no significant advancement on the ground. In late 2023 the company rebranded to Koryx Copper Inc.

In mid-2024 new leadership took over: Namibian-born engineer Heye Daun (former President of Auryx Gold and Osino Resources, with multiple +C$100M exits in Namibia) became Executive Chairman, and mining lawyer Alan Friedman (co-founder of those ventures) joined as Lead Director. They immediately injected capital (multiple private placements), hired technical experts, and reset strategy. Under their stewardship, Koryx raised roughly C$18.0M at C$1.10 in Nov 2024, followed by other funding rounds.

Today Koryx has ~67.7M shares outstanding (82.9M fully diluted) with no significant near-term debt. Insider/management ownership is about 10% (acquired via placements and market purchases), aligning interests. Other prominent shareholders include Ross Beaty’s group, Mackenzie, RCF, Extract Capital, Commodity Discovery Fund, and Teck Resources (which retains ~7% passive stake). With ~C$17M cash on hand after the latest financing, the company can fund its 2025 drilling and engineering programs.

Management & Ownership Analysis

The Koryx board and team are built on seasoned Africa mining veterans. Heye Daun (Executive Chairman) is a mining engineer with a 25-year track record of successful project development and exits in Namibia and Ghana (e.g. selling Auryx Gold to B2Gold for C$180M, and Osino Resources to Shandong Gold for C$368M). Alan Friedman (Lead Director) is a long-time corporate lawyer and capital markets specialist who co-founded Osino and Auryx with Daun.

Supporting them are technical experts largely from their Osino team: for example, Charles Creasy (Head of Project Development) and Steve Burks (Senior Metallurgical Consultant) who were instrumental in Namibia projects, and a new COO, Trevor Faber (formerly COO of Alphamin Tin in DRC). In sum, over 80% of Koryx’s management and board are Osino alumni, implying strong continuity and local experience.

This management team is further backed by major mining investors. The Dec–Nov 2024 financings were heavily oversubscribed and were joined by strategic funds. Insider ownership stands at ~10%, which is healthy for alignment. No warrants were attached to the latest rounds, reflecting discipline on shareholder dilution. The strong shareholder list and fresh capital suggest both belief in the project’s potential and confidence in the new team.

Haib Copper Project

Location & Infrastructure:

Haib is in Namibia’s Karas Region, near the Orange River and border with South Africa. The site is low-elevation and proximate (tens of km) to roads, grid power and potential water supplies. Namibia is considered mining‑friendly: it is a stable democracy with transparent mining laws and favorable fiscal terms (37.5% tax rate and a 3% royalty)

The project's infrastructure advantages are particularly noteworthy. Located at a relatively low altitude, the site is within 20 kilometers of essential utilities, including roads, grid power, water supply, and well-serviced towns. The company has engaged in discussions with the Water Affairs to secure water access to a potential pipeline from the Orange River, with an estimated annual demand of 2.4 to 5 million cubic meters depending on the final process plant design. Other mining projects such as Rosh Pinah Zinc and Skorpion Zinc have a water access right to the Orange River.

Geological Setting:

Haib is a Paleoproterozoic copper-moly porphyry deposit – one of only two known porphyry copper deposits of this age in southern Africa. The mineralization is predominantly chalcopyrite (with lesser bornite, chalcocite) and contains significant copper and minor gold and molybdenum.

Because of later metamorphism, much copper is still primary (not oxidized). The deposit exhibits classic porphyry features (multiple mineralized zones and alteration shells). Drilling to date (historic plus Koryx’s 2024 program) has demonstrated continuity of mineralization over a large area and to significant depth.

Historical work & Scale:

Haib’s exploration history dates to the late 1800s; Falconbridge, King Resources, and Rio Tinto all drilled extensively (over 78,000 m total by the 2010s). Teck Resources completed a drilling and study program up to 2015 before exiting Namibia. The recent 2024 NI 43-101 technical report (effective Aug 31, 2024) reports a total resource of 414 million tonnes Indicated @ 0.35% Cu and 345 million tonnes Inferred @ 0.33% Cu (0.25% cutoff)

The Indicated resource grade is 13% higher than in 2021’s estimate, despite a 9% lower tonnage, meaning overall contained copper rose ~3% year-over-year. These figures place Haib among the largest undeveloped copper deposits globally; comparably sized porphyries typically lie in copper‑rich districts like Chile, Arizona, and Mongolia.

Jurisdiction:

Namibia consistently ranks as one of Africa’s most attractive mining jurisdictions. Recent events reinforce this: a Namibian High Court in March 2023 upheld Koryx’s Haib licence, vindicating the rule of law.

Namibia is a stable democracy with a well-established mining industry that contributes 8% to the country's GDP and 40% to its foreign earnings. The country offers a transparent system of mineral title, predictable permitting processes, and favorable fiscal terms including a 37.5% tax rate and 3% royalty.

The government has since been cooperative, and local mining policy encourages foreign investment in copper. Management points out that Namibia’s stable politics, mining experience (Zinc mines like Skorpion, Rosh Pinah), and transparent permitting system all favor project development.

Project Economics & Upcoming Catalysts

Updated PEA (2025):

Koryx is assembling a revised Preliminary Economic Assessment (PEA) for Haib, targeting release in Q3 2025. The base case will evaluate a conventional open-pit mine with crushing/milling/flotation, producing copper concentrate, plus a potential heap-leach expansion to extract lower-grade ore by solvent extraction-electrowinning (SX/EW). Early metallurgical testwork (grinding, flotation, sorting, leaching) has been very encouraging: e.g., average copper recoveries of ~89% in flotation to a 20–25% Cu concentrate

Historic Mintek 1996 flotation results are being matched or exceeded, and a heap-leach scoping (column leach) has begun. Engineering consultants from South Africa and Chile (DRA, Mintek, Maelgwyn, etc.) have been engaged to verify flowsheet design. Drill core from the highest-grade portions (>0.275% Cu) is being processed to optimize recovery. All testing necessary for the PEA (except extended leach tests) will be completed by mid-2025.

Publication of the PEA in Q3 2025 is a major event – it will define the project’s cash costs, capital needs, and baseline NPV/IRR. A high-quality PEA may significantly de-risk the investment case; conversely, any surprising costs (e.g. power, water infrastructure) will be revealed.

Drilling Programs:

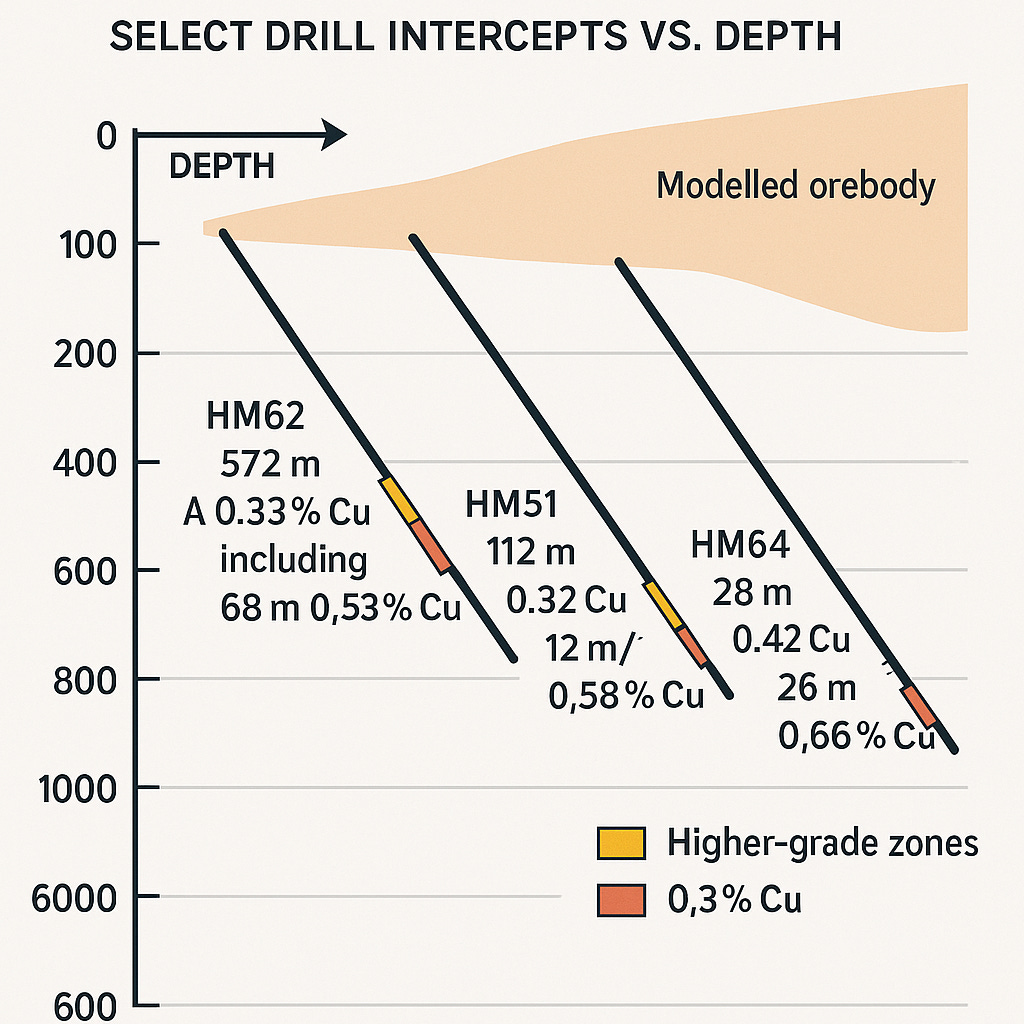

Koryx launched a multi-phase drilling campaign in 2024–25. In Q4 2024 they completed Phase 1 infill drilling (18 holes, targeting high-grade shoots). Phase 2 (ongoing) plans ~37 holes (~8,600 m) focusing on zone extensions and continuity. As of late May 2025, 29 holes (8,647 m) were done, with assays from 12 holes reported (3,603 m).

These results are very positive: many holes returned copper grades above the current resource average (for example HM62: 572 m @ 0.33% Cu, including 68 m @ 0.53% Cu; HM51: 112 m @ 0.32% Cu with 12 m @ 0.58% Cu; HM64: 28 m @ 0.42% Cu and 26 m @ 0.66% Cu).

These wide, higher-grade intercepts suggest the deposit may be bigger and richer than currently modelled, especially near the vertical shear zones. Based on these encouraging results, Koryx plans to ramp up drilling: 4 rigs are operating now, with 4 additional rigs to arrive in Q3 2025. The full program for 2025–early 2026 totals ~55,000 m of diamond drilling

Continuing drill results will help upgrade the resource and potentially expand the mineable envelope. Koryx plans a new Mineral Resource Estimate in H1 2026 and a follow-on technical study (PFS or updated PEA) that incorporates all new data.

Permitting & Infrastructure:

With drilling and testing underway, the company is advancing permits and engineering studies. A mining license application has been submitted and is under review. Environmental and social impact studies (ESIA) are led by Knight Piésold, with community engagement ongoing. No major roadblocks have been reported.

Studies of power and water have quantified requirements: the base-case milling operation needs ~120 MW and ~20 million m³/year of water, which appear achievable given regional utilities and planned Orange River access. Tailings management options (thickened tailings to on-site storage) have been evaluated.

Approval of key permits (mining licence, ESIA) – expected by 2026 – is critical. Demonstrating community support and a viable infrastructure plan will be important for investors.

Other Assets (Zambia):

Beyond Haib, Koryx holds two exploration licenses in Zambia’s Copperbelt (Luanshya West and Kalaba North). These are early-stage, geophysical/anomaly targets. Recent drilling has identified copper and cobalt anomalies, and some maiden soil samples have been reported, but these projects are far from development.

Koryx says it will complete these 2025 regional programs (geophysics, drilling) while Haib remains the focus. These Zambian assets provide optionality (tier-1 mining region) but are not central to the near-term thesis.

Risk Factors:

Grade and Scale:

The deposit’s grade (~0.34% Cu) is lower than many greenfield mines. Koryx must move very large volumes of rock to generate meaningful copper output. This inherently makes capital and operating costs high per unit metal, and leaves less margin for error. If metals recoveries fall short of expectations (despite encouraging tests), it could materially affect project economics.

Financing:

Management acknowledges it will “require additional funding to complete further development work” on Haib. While ~$17M cash currently funds drilling and PEA, a full Feasibility Study and mine construction (if decided) would need hundreds of millions. Success will depend on raising these funds at reasonable cost. If markets sour or Koryx’s share price stalls, future financings could dilute existing shareholders or be hard to close.

Permitting:

Although the critical mining license was renewed, Koryx still needs environmental permits and water/power rights. Any protracted permitting or opposition could delay or add costs. For instance, securing the Orange River water license is not guaranteed. However, Namibia’s track record and Koryx’s engagement (e.g. ESIA contractor hired) mitigate but do not eliminate this risk.

Jurisdiction:

Namibia is stable by African standards, but it is not a Tier-1 jurisdiction like Canada or Scandinavia. Political change or policy shifts (e.g. changes in mining code or taxes) remain a remote risk. That said, management emphasizes Namibia’s transparent title system and legal predictability; the 2023 court win over the Haib license underscores that rule of law.

Other:

Typical junior/mining risks apply – currency fluctuations (though copper sales will be USD), inflation on equipment costs, weather or logistical delays, and commodity cycles. Koryx has no revenue or hedges, so it is fully exposed to copper price swings.

Valuation

Koryx is pre-revenue, so valuation has to rely on asset and resource value, plus execution. At ~C$0.90–C$1.10 per share (mid-2025 range), Koryx’s EV is only a few tens of millions of USD. That is strikingly low relative to the contained copper (~3.5+ billion pounds), hence the low EV/lb metric. This disparity reflects the early stage and remaining risks. For institutional investors, the implicit “option value” is large: if Koryx delivers on its catalysts, the share price could rerate substantially.

We note management’s own guidance: with >C$17M cash, the company can finish drilling and PEA by late 2025. A positive PEA (with IRR above threshold) could reprice the stock. Conversely, a disappointing PEA or drilling campaign could flatten the valuation. Detailed DCF or NAV modeling is not yet possible without PEA inputs (capex, opex) and final mine plan.

However, one can roughly back into an implied resource value: for example, if global copper development peers trade at ~C$0.05–0.10 per pound of contained metal, Koryx’s 3.5B lb implies potential well over C$150M valuation in a full-funding scenario (vs current ~C$80M EV). This simplistic math underscores the “deep value” argument. Of course, we await actual economic projections. In summary, Koryx’s current market valuation appears conservative given its large resource and progress, but realizing value hinges on execution of studies and raising next-stage capital.

Conclusion and Investment Thesis:

Koryx Copper offers investors a leveraged play on copper through a massive, high-potential project and strong execution team. The key bullish points are:

(1) Project scale and quality: Haib’s vast resource and geologic merit are rare (one of the largest undeveloped porphyries, with resource upgrading in 2024).

(2) Proven management: Daun and Friedman (and team) have repeatedly built and sold Namibian mines, and are now focused exclusively on Haib.

(3) Advancing catalysts: ongoing drilling and a PEA by Q3 2025 (plus Namibian listing and Zambia exploration) should provide newsflow and de-risking in the next 6–12 months.

(4) Favorable macro: copper prices remain strong, so even conservative economics look robust, and future demand (EVs, grids) underpins long-term viability.

The downside considerations are clear but manageable: the project’s low grade requires scale (meaning big capex), so financing will be heavy and dilutive unless managed prudently. Permitting or technical setbacks could slow progress, and copper prices could wobble in the short term. Nevertheless, with a market cap well below what one would expect for an asset of this size, Koryx appears to offer significant upside potential for patient investors.

We recommend Koryx as a speculative buy for investors seeking pure-play copper exposure with embedded upside. The combination of a massive resource, world-class management, and near-term milestones (drill results and a formal PEA) creates a compelling narrative.

Key performance triggers include continued high-grade drill intercepts (which seem likely given results to date) and a positive PEA confirming attractive economics. If these catalysts are met, Koryx’s share price could re-rate toward peer levels. Conversely, failure to deliver on studies or capital could significantly hurt the valuation.